Click here for the new Anchor Rising & Ocean State Current page

Click here for the new Anchor Rising & Ocean State Current page

Union Rules and "Unique System" Drive Up Overtime for State Government Community Living Aides, by Justin Katz

Labor

11:00 AM, 04/17/13

Redistributive Property Taxes: Who's in the Providence Crosshairs?, by Justin Katz

Taxation

12:54 PM, 04/13/13

Property Tax Assessments, by Patrick Laverty

Taxation

10:15 AM, 04/12/13

UPDATED - Providence: 8th Highest Residential Tax Burden in the Country (Commercial Taxes Even Worse), by Monique Chartier

Taxation

9:55 PM, 02/16/13

02/13/13 - Senate Finance Committee, Sakonnet River Bridge Tolls, by Justin Katz

Taxation

4:59 PM, 02/13/13

When the Insiders' Cut Comes First, by Justin Katz

Taxation

8:04 AM, 01/30/13

Hm. Maybe the Status Quo Option Will Work for RI, by Marc Comtois

Taxation

3:30 PM, 01/16/13

Legislation Under the Radar - Mo' Money for the General Fund, by Justin Katz

General Assembly

8:48 AM, 01/16/13

Burying the Legislative Lead, by Justin Katz

General Assembly

4:37 PM, 01/15/13

GOP and Sales Taxes, by Patrick Laverty

Taxation

9:00 PM, 12/27/12

April 17, 2013

Union Rules and "Unique System" Drive Up Overtime for State Government Community Living Aides

Suzanne bates has another state-payroll-related investigative report on the Ocean State Current, this one covering a job titled "community living assistant."

These are high-school-educated employees with average regular pay below $36,000, who've been able to triple their pay with overtime and other salary enhancements, topping out near $130,000. Their job entails helping the residents of group homes, with at least two CLAs watching over four to six patients on a 24-hour basis. Obviously, there's apt to be downtime.

Especially notable, in this case, is the role of union rules in driving up the overtime costs. A decade ago, the department attempted to introduce "floaters," who could cover shifts at more than one of the facilities. The union objected that the strategy wasn't fair. On the other hand, senior CLAs can effectively "float" around the state... as long as they're doing it for overtime.

As we continue to sort through the outrageous spending for which so of Rhode Islanders' income is confiscated through taxes, Suzanne's doing a great job of filling in the picture of how the game works.

April 13, 2013

Redistributive Property Taxes: Who's in the Providence Crosshairs?

The way property taxes work, in Rhode Island, revaluations are little more than a way of redistributing the tax burden, and in Providence, a shift from taxing buildings to taxing land has repercussions for a number of recent issues, from the Superman Building to legislation affecting the entire state.

April 12, 2013

Property Tax Assessments

Based on some Twitter chatter this morning, I learned that the property tax assessment letters are going out today in Providence. The citizens of our capital city are learning what value their homes and land will be taxed at. There is always some confusion as to what this means.

First, the city should be using a value that they think is the current fair market value for the land and the building on it. This should be approximately what the property would sell for on the open market. I've seen many times when these aren't even close, especially in my own town and my own property. I tried selling mine for nearly $30,000 less than the assessed value and I couldn't even get an offer. My solution to this would be to require the town or the company doing the assessing to purchase the property at this assessed price, if the owner is willing to sell, within 30 days. I'm guessing the property values would be set much more closely to what is realistic at that point.

But what do these values mean? If your assessed value goes down, does that mean your property taxes will go down too? Not likely and in most cases, they'll actually go up. They go up because the town still needs (or thinks it needs) additional revenues every year. Employees get raises, services and goods like electricity, heating oil, natural gas, are all things that cost more.

The way a city derives your tax bill is actually in two pieces. Neither piece means anything by itself. It's a combination of the assessed value and the tax rate. According to RILiving.com, the last property tax rate for non-commercial property was $31.89 per $1,000 of assessment. If your property is assessed at $300,000, simply mutiply that $31.89 by 300 and you get your property tax bill of $9,567 per year. However, Providence does offer a homestead exemption. This means if the property is your primary residence, Providence cuts that bill in half. Well, unless you're the Governor, then you can live anywhere you want and still get the homestead exemption.

Seems pretty straightforward. The town has their rate, does their assessments and that's their revenue. This would seem to be a problem if the property values drop at all. That would mean less revenue for the city, right? Nope. The cities actually do these calculations in reverse. In a way that might not really make sense. First they figure out how much money they need for everything they want to do and everything they want to support. Next, they take the total assessed value, divide one by the other and the result becomes the tax rate.

In a nutshell, your assessed value going down really doesn't mean anything at all. You need to take both values, assessment and the tax rate into effect. Because the city doesn't want to have a decrease in revenues along with the decrease in assessed value, they will in turn either increase the tax rate, lower or eliminate the homestead exemption or some combination of both.

February 16, 2013

UPDATED - Providence: 8th Highest Residential Tax Burden in the Country (Commercial Taxes Even Worse)

Funny that this should pop up now. (Major H/T Michael Graham. By the way, welcome back to the air, Michael. We missed you.)

It's the reason that I haven't shared the enthusiasm [link added] for the ... um, fiscal "achievements" of Mayor Taveras' tenure, genuinely nice guy though he is. His pension reform, as tepid as the state's, has only succeeded in locking Providence taxpayers into the eighth highest taxes in the country. Block Talk Editor Jenna Bromberg reports.

The tax burden of taxpayers living in different parts of the United States varies due to differences in state and local income taxes, property taxes, sales taxes and automobile taxes. So how does your city stack up?Drumroll please…

The top ten cities* with the highest tax burden for a hypothetical family of three making $50,000 in 2011:

#10 Boston, MA

Paul Revere made his famous midnight ride on horseback here — but today, trading in the horse for a car of your own would cost $303 in taxes per year. The total tax burden for our hypothetical family in Boston sits at 12.2%, or about $6,125 annually.

#9 Burlington, VT

Vermont’s largest city, home to the very first Ben & Jerry’s, was ranked by Forbes as one of the prettiest towns in America — and we’re sure its 42,500 residents agree. But at a 12.3% tax burden ($6,150 per year), it’s #9 on our list of the most taxed cities in America.

#8 Providence, RI

The city of Providence is known for its historic and cultural attractions; it was first settled in 1636 by Roger Williams and was one of the original Thirteen Colonies. As of the 2010 census, 178,042 people lived within the city of Providence — and our hypothetical family paid $6,034 in taxes in 2011. $3,876 was property tax alone.

Yes, undoubtedly, backing down a substantial tax burden cannot be carried out in one term. But let's save the praise for when the burden is lessened, not just stabilized - especially when "stabilized" means assuring our position on yet another undesirable Top Ten List.

ADDENDUM

That, of course, is the residential tax rate. We would be remiss if we did not note that Providence's commercial tax rate - second highest in the country - is even higher. When do we start addressing both of these absurdly high burdens?

[Monique is Editor of the RI Taxpayer Times newsletter.]

February 13, 2013

02/13/13 - Senate Finance Committee, Sakonnet River Bridge Tolls

Justin writes live from the Senate Finance hearing on repealing the Sakonnet River Bridge toll.

January 30, 2013

When the Insiders' Cut Comes First

Even if you've disagreed with everything I've ever written, take a moment to ponder the thinking on display in this Kathy Gregg article. It's about a study from the left-wing Institute on Taxation & Economic Policy finding that Rhode Island places a high tax burden on lower-income families.

January 16, 2013

Hm. Maybe the Status Quo Option Will Work for RI

Offered entirely tongue in cheek...I think.......Anyway, it looks like Governor Patrick is going to propose a series of tax hikes that could end up making Rhode Island look good in comparison (shhhhh, don't tell anyone!):

According to Boston.com, Patrick listed possible revenue sources including:Of course, my guess is that our leaders oft-stated goal of trying to be more like Massachusetts will finally take hold once these proposals get through!Raising the gas tax from 21 cents to 51 cents per gallon

Raising the sales tax from 6.25 percent to 7.75 percent

Raising the state income tax to 5.66 percent from 5.25 percent

Levying a vehicle miles-traveled tax at 2.4 cents per mile

New, emissions-based vehicle title and registration fees could raise $175 million

A payroll tax on workers in regions with transit service could raise $140 million to $207 million

Legislation Under the Radar - Mo' Money for the General Fund

I'm going through all legislation as it's introduced to the Rhode Island General Assembly, and the Center for Freedom & Prosperity will be putting out a real-time Freedom Index — essentially a watch list — in a couple of weeks. That'll have the collection of good and bad within the think tank's scope.

Card check? Check. Master lever? Yup. Mail ballots for lazy voters? Uh-huh. General Assembly term limits? Absolutely.

But in keeping with yesterday's post about overly discreet legislation concerning Bryant's taxes, I'm not able to resist mention of bills that I find intriguing, including those that are of interest because of the way they're presented.

January 15, 2013

Burying the Legislative Lead

Most legislation introduced into the General Assembly comes with a brief summary that appears with references to the bill — most visibly on the various pages of the legislature's Web site. Sometimes the descriptions are misleading; sometimes they're just confusing. (Usually, they're pretty good, assuming one understands the lingo of policy.)

Today, Representatives Thomas Winfield (D, Smithfield, Glocester) and Gregory Costantino (D, Lincoln, Smithfield, Johnston) submitted legislation with a description that puts a superficial effect first and excludes the most significant purpose of the bill from the locations where it would be most easily spotted.

December 27, 2012

GOP and Sales Taxes

It seems the RI Republicans in the State House might be finally stumbling on to an idea they can hang their hats on. Eliminating the state sales tax. Granted, it's one that they may be simply saying "me too" on as the RI Center for Freedom and Prosperity suggested this back in June. However, that's the whole point. The reason for places like this Center is so they come out with reasoned and researched ideas and then the legislature can decide which ones make sense and move them forward.

This type of idea is exactly the kind of bold thinking that the GOP needs to jump on. This is the party that can't even come up with a unified platform, but if they could forget about all the silly internal bickering they seem to get involved with and rally around an idea like this and sell it to the people of the state, from the leadership to every town committee, it's something that they could possibly see advanced.

Some are having difficulty understanding how eliminating the sales tax can help the state after about $880M of revenue is brought in through this tax. Even if businesses were to boom with the elimination of the tax, a trillion dollars multiplied by zero percent is still zero. But, if you need any evidence in seeing what a lower sales tax can do, look no further than Attleboro and Seekonk. It's no coincidence that so many stores are sitting right on Rhode Island's borders. If Rhode Island were to go to zero sales tax, we'd gradually see these stores move across the border and into the state.

But how would the state cope with the loss of the $880M in lost sales tax revenue? Well, for one, it's not that much, it's only about half of that when you don't count the gas tax, tobacco tax and meals tax that would remain in effect, according to the actual report on the Center's site. They also claim somewhere between 50 and 70% of the lost revenue would be reclaimed on the increased business presence in the state and the additional income tax revenues. If you have more business, you have more jobs and with more jobs, you have more income tax. The Center advocates for the remaining 30-50% to be made up through cuts to the state's services and even eliminating about $7M just by downsizing the state's tax collectors and tax enforcement agents.

I believe that many perceived and real problems go away when people have a job and have income. If we have businesses in the state, people will have jobs, people will have money, people will buy homes in the state, property values will finally increase and municipalities will be able to turn around many of their financial woes.

Finally, here is an idea that the state Republican party can actually get behind, do the work and get all the numbers. Make an intelligent and reasoned case to the people of the state, put on an election-like campaign blitz and then let others explain why we should all pay 7% on top of the cost of goods. Even better, this would get people to stop shopping in Massachusetts and keep the money in Rhode Island, for Rhode Island.

December 8, 2012

Mortgaging the Economy

Marc Comtois highlights another fascinating glimpse into the reasoning behind policy ideas that he and I agree are, well, in error. I'm speaking of this paragraph from Slate's Matthew Yglesias:

... I'm especially enthusiastic about the mortgage part. Suppose homeowners in expensive coastal cities couldn't deduct their mortgage interest, what would happen? Well, what would happen is that prices would fall. But nothing more dramatic than that. All the deduction does is encourage further bidding up of the price. In a normal market, that bidding up of the price might lead to additional construction. But the main reason those blue metro areas have such expensive houses is that zoning doesn't allow demand to be matched with supply. No matter how expensive Georgetown or Harvard Square or Park Avenue gets they're not demolishing the existing structures and replacing them with much larger ones. So you'd get some extra tax revenue this way with no real change in the amount of underlying economic activity.

Look, I've been known to make statements about the effects of policies that are arguably over-confident, but at this level of detail, human behavior has a definite x-factor of which policymakers (and policy-propounders) should beware.

December 5, 2012

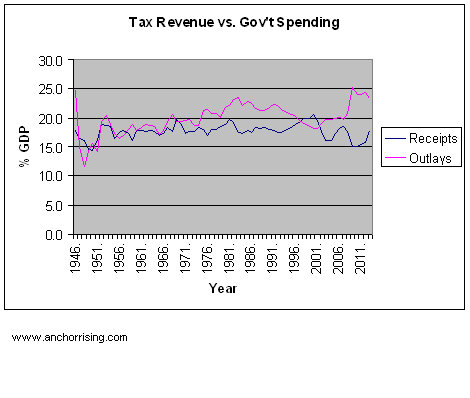

Stop Spending

As Michael Barone points out, historically, no matter the tax rate, tax receipts have almost never eclipsed 20% of GDP. The only time they did (20.5%) was in 2000 just before the dotcom bubble burst. Here's the chart:

Source: Economic Report of the President 2012, Appendix B, Table B-79, p. 412.

As Barone explains:

In the Obama years, federal receipts have hovered at 15 percent of GDP.Any serious economic plan has to reduce spending to below 20% of GDP because receipts just aren't going to get above 20% of GDP. But no one is interested in being serious.That's just because tax rates are too low, Obama backers reply. Just raise the rates on high earners and the problem will be solved.

Actually, high earners don't make enough money to close the current budget deficit. You'd need to raise taxes on middle-income earners too.

But we have had higher income tax rates in most of the years since World War II. What history and Table B-79 show is that even much higher rates -- like the 91 percent marginal rate on top earners imposed from the 1940s to the 1960s -- have never produced federal receipts higher than 20 percent of GDP.

Why is that? As the late Jack Kemp liked to say, when you tax something, you get less of it. When the government took 91 percent of what the law defined as adjusted gross income over a certain amount, not many people had adjusted gross income over that amount.

According to a Congressional Research Service study, the effective income tax rate on the top 0.01 percent of earners in the days of nominal 91 percent tax rates was only 45 percent. Others have pegged it at 31 percent.

In the 1970s, when the top rate on wage and salary income was 50 percent and 70 percent on investment income, high earners spent much of their time and energy seeking tax shelters. The animal spirits of capitalists, to use John Maynard Keynes' term, were directed less at productive investment and more at tax avoidance.

ADDENDUM: And, for the umpteenth time, any proposed spending "cuts" aren't cuts at all, just a reduction in the projected amount of increased spending.

November 28, 2012

Things We Read Today (36), Wednesday

Threats to the economy (cliffs and debts); RI lagging again (yawn); dependors and dependees; Social Security a problem; and a civil right to the war zone frat party.

November 21, 2012

To Starve or Gorge the Beast?

"[W]e've got to reduce spending before we can reduce taxes. Well, if you've got a kid that's extravagant, you can lecture him all you want to about his extravagance. Or you can cut his allowance and achieve the same end much quicker. But Government has never reduced. Government does not tax to get the money it needs. Government always needs the money it gets." ~ Ronald Reagan

Hence was born the idea of "starve the beast," a conservative core belief if ever there was one. But is it true? As explained in a recent column by Andrew Ferguson, economist (and libertarian) William Niskanen didn't think so.

Beginning in 2002, Niskanen published a series of papers and op-eds about tax cuts and spending increases that turned conventional conservative wisdom on its head....If we wanted a smaller government, he said, we would have to raise taxes....Niskanen, looking over 25 years of budget data, noticed something about STB ["Starve The Beast" ~ ed.]: It didn’t work. In fact, attempts to starve the beast by tax cuts seemed to lead to increased federal spending.That last--the ability of government to write checks on credit--was overlooked by STB advocates.Niskanen looked at both spending and taxes as a percentage of GDP. On average, he found, if federal revenues declined by 1 percent, federal spending increased by 0.15 percent. When revenues rose, on the other hand, relative spending decreased. A further study in 2009 by another Cato economist, Michael New, came to the same conclusion after the gluttonous administration of George W. Bush. Under Bush and his mostly Republican Congress, new benefits like subsidized Medicare drugs and increased federal education spending followed on the heels of large tax cuts.

Niskanen’s explanation for the failure of STB was straightforward, a conjecture based on standard economics: When you cut the price of something, demand for it will increase. Lowering taxes without lowering benefits meant that taxpayers were getting the benefits at a discount. The government made up the true cost with borrowed dollars that future taxpayers would have to repay. There was a big difference, Niskanen said, between a kid on an allowance and the federal government: The government has a credit card with no debt limit. {emphasis added}

[E]arly advocates of STB had counted on something that never materialized. They had assumed that as the debt piled up to finance annual budget deficits caused by free-flowing benefits, public outrage would force politicians to restrain spending without raising taxes. Yet we’ve had the deficits and the borrowing, in amounts that would have left Friedman and Reagan agog; what’s been missing is the outrage.People aren't outraged because they don't feel the immediate pain of increasing government because the money for government expansion is either borrowed or paid for by increasingly fewer individuals. So around 50% of the population feels no pain (they don't pay income taxes) while a majority of the rest pays relatively minimal amounts. And a lot of that pain is left to future generations. This aligns with Niskanen's reasoning for why higher tax rates lead to lower spending:

“Demand by current voters for federal spending,” he explained, “declines with the amount of this spending that is financed by current taxes.” When you make them pay for government benefits out of their own pockets, in other words, voters will want fewer of them. The journalist Jonathan Rauch put Niskanen’s point more pithily: “Voters will not shrink Big Government until they feel the pinch of its true cost.”Yet, as I mentioned, not everyone shares the tax burden evenly in our progressive income tax system. So, perhaps a flat tax would prove or disprove Niskanen's theory, but it's doubtful that will happen any time soon.

Ferguson's article brought some critiques of Niskanen's ideas. Noah Glyn offers up another reason for why government spending decreases when tax revenue increases:

[It's] the business cycle. As the economy grows, people earn more so they pay more in taxes; conversely, when the economy enters a recession, government revenue plummets. During recessions, however, the public relies on increased government spending, in the form of Medicaid, food stamps, and other transfer payments. (This can go the other way, too: Some state and local governments have used economic growth to justify increasing promises to government employees’ pension plans, but those costs typically come much further down the line.)This is buttressed by Ramesh Ponnuru's important, technical point and "thought experiment":

Let’s say we still had the Clinton-era tax rates and a (smaller but still quite large) long-term debt problem. Wouldn’t we be debating an increase in tax rates to a higher level than we are now? That seems to me pretty likely. The baseline from which we’re negotiating would be higher, perceptions of what’s tolerable would be higher, expectations of tax rates would be higher. On the Niskanen theory there would be a countervailing effect: In the interim the tax cuts caused spending to be higher and thus moved the spending baseline higher. But Niskanen didn’t find that a dollar of tax cuts were associated with a dollar of spending increases; he found that a 1 percent reduction in revenue over GDP was associated with a 0.15 percent increase in spending over GDP. So the countervailing effect would be smaller.Jonah Goldberg adds:

I always liked Niskanen’s argument, even if I didn’t quite find it persuasive. One thing that always bugged me about it which, to my surprise, Ferguson doesn’t mention, is the implicit assumption that Americans behave like rational economic actors with regard to what they get from government....The American species of homo economicus has been paying hundreds of billions to get rid of poverty for decades, what do we have to show for it? Poverty rate in 1975: 26 percent. Poverty rate in 2010: 26 percent. What a great return on the investment. Federal spending on education? Ahem...For reasons, good and bad, voters don’t treat tax dollars the way they do their own dollars. They don’t demand quality. They don’t demand accountability. They don’t push for efficiency. Many people think the government should spend money as if it comes from someplace other than the wallets of citizens and that what we get for it should be graded on some spiritual, emotional, philanthropic or metaphysical curve. How we spend for X so often seems to matter more than how much X is actually delivered.Yet, as Patrick Brennan argues, re-stating Niskanen's implicit premise, the missing demand for government quality is because so many have so little stake in the game.

People might be a lot more likely to start caring about where their tax dollars go (whether the ends are efficient and whether the money comes back to them) when those taxes are really substantial, broad-based, and they actually have to pay them.Brennan also compares U.S. expectations for government services to that of Europeans:

If you live in a society where, as Jonah pointed out Arthur Brooks has argued, the state is considered the main conduit for meeting societal needs and caring for the poor and vulnerable, you’ll care more about how well government works and whether it can care competently for you, and that’s a cultural matter. But it’s also important to homo economicus, because Leviathan has taken most of his paycheck, and he now has to hope, and should ensure, that government will provide for society at large, the poor and vulnerable, and even him at times, and do so as efficiently and competently as possible.Regarding the last, many conservatives (well, at least me) believe that a smaller government is one that is easier to make workable!There are obviously other explanations for these differences: Charlie Cooke has lamented to me on many an occasion that in Britain, the conversation about almost all government policies ends up being debates over efficacy of programs, not whether the programs should exist in the first place. Leaving aside the financial constraints Britain and elsewhere are now experiencing, if you don’t have a constitution with enumerated federal powers, a truly conservative and independently minded political movement, etc., you’re going to spend more time on making government work, not on making it smaller, and that’s for other reasons than I’ve just proposed.*

==========================

* Brennan expounded on the point later in the post: "It’s difficult to assess my thesis inasmuch as big government and the cultures that give rise to it have other negative effects on efficiency, so it’s possible citizens subject to a huge government and a regressive tax code get a more efficient government than they would if they didn’t have higher expectations than free-riding Americans, but still not a very efficient one. It’s been suggested, in fact, that it’s highly efficient yet regressive taxation (like light capital taxation, competitive corporate-tax rates, consumption taxes, etc.) that’s allowed places such as France and Scandinavia to have functional economies despite the burdens of absurdly large governments; perhaps it’s also the relative efficiency and usefulness of their government spending programs, and not just their tax system, that’s allowed them to manage as well. Thus again, economic preferences force the hand of citizens and politicians in a completely government-dominated society but not in one like America."

October 24, 2012

Things We Read Today (26), Wednesday

Mainly on government's bad incentives: bad housing spending in Providence, unlearnable spending lessons for the governor, stimulus corruption, and Medicaid reform.

October 10, 2012

Cato Gives Governor Chafee a D in Fiscal Policy

In a white paper out yesterday from the Cato Institute, Governor Lincoln Chafee (as the chief executive of the Rhode Island government) received a score of D for fiscal policy. His score of 41 is based on spending, revenue, and tax changes that he proposed and/or that were implemented under his watch from January 2010 to August 2012, and marks him as the seventh worst governor for fiscal policy.

September 28, 2012

Tiverton Toll Meeting Shows Rhode Islanders Have to Stop Fighting Fire with Paper

Last night, I attended the first organizational meeting for the Tiverton branch of Sakonnet Toll Oppostion Platform (STOP), a cross-community effort to stop the state of Rhode Island from placing a toll on the Sakonnet River Bridge. If I was skeptical about the ability of residents to prevent the tolls before, I'm pretty well convinced that the people of the East Bay will not be able to stop them, now.

The audience consisted of approximately fifty residents, from a broad variety of local groups and interests — many most often seen in heated attacks against each other over the usual slate of issues that face the town. Even though the only state-level official in the room was Sen. Walter Felag (D, Bristol, Tiverton, Warren), the opportunity should be there, in other words, for some effective leaders to draw on the strengths of the different groups to affect state-level lawmakers.

Instead...

September 24, 2012

Even a 100% Tax on Millionaires Wouldn't Close Federal Deficit

"Even if the government took all of the income earned by those who have an after-tax income of $1million or more, the amount of revenue generated would fall far short of eliminating the deficit."

September 20, 2012

House Makes it easier for Buffet, billionaires to pay down Federal debt

The House of Representatives--on a bi-partisan voice vote--passed the "Buffet Rule Act", which allows anyone to voluntarily pay more in taxes.

Under the legislation, which would still need Senate approval, taxpayers could check a box on their taxes and send in a check for more than they owe to the IRS."If Warren Buffett and others like him truly feel they're not paying enough in taxes, they can use the Buffett Rule Act to put their money where their mouth is and voluntarily send in more to pay down the national debt, rather than changing the entire tax code to inflict more job-killing tax hikes on hard-working Americans," said Rep. Steve Scalise, the Louisiana Republican who wrote the bill....Current law already allows taxpayers to send money to pay down the debt, but Republicans said that process is onerous. Under their new plan, taxpayers would have an easy option on their tax returns allowing them to pay more.

Under Republicans' legislation, the money would go directly toward reducing the debt.

September 3, 2012

Things We Read Today, 1

One thing I've learned, in years of blogging, is to be wary of proclaiming new regular features. Yet, I've been finding myself at the end of each day with a browserful of tabs of content on which I'm inclined to comment.

So, as interest and time allow, I'll publish quick-hit posts containing commentary that is somewhere between a tweet and a full-on blog post.

Leaning Against the Privileged Place of Investments

Readers shouldn't be surprised to hear that I'm largely in agreement with Peter Ferrara's "Obama's Accelerating Downward Spiral for America," but he happens to voice one bit of center-right common wisdom with which I have growing disagreement:

There is no secret or magic as to how to turn around these declining incomes. Increased investment in business expansion and start ups increases demand for labor, which drives up wages. That investment buys new tools and capital equipment for workers, making them more productive, which provides the cash flow to increase wages.Increasing investment results from reducing the tax rates on investment, which enables investors to keep a higher percentage of what they produce, increasing incentives for investment.

My resistance to this suggestion — notwithstanding Ferrara's positioning of it as a statement of the obvious — has three sides.

August 27, 2012

Note To GoLocalProv: RI "Rich Pay Less In Income Tax" = Third Highest Income Tax Rate In Country

GoLocalProv's Dan Lawlor has a column today in which he attempts to causatively link Rhode Island's top income tax rate to our unemployment rate.

In 1997, during a boom economy in RI- remember the Renaissance? - the top income earners had a 27.5% income tax rate. Our jobless rate was 5.3%.

Ah, but then, in 2010, according to Dan, we hit the skids, both in unemployment and top tax rate-wise.

In 2010, the General Assembly and Governor Carcieri reduced the top income tax rate from 9.9% to 5.99%. The state's sales tax remained at 7%. Our unemployment rate was 11.6%.

Uh huh. Two years later?

Top income earners now pay 5.99% in income taxes. Our jobless rate is 10.8%.

And the conclusion (according to Dan)?

Our tax policy has basically been that the rich pay less in income tax, and we all pay more in property and sales tax.

We could at this point ask if perhaps ALL of Rhode Island's taxes aren't too high and if this situation isn't most likely a direct result of too much spending on the state and local level. But we'll stick to what Dan wrote, only, if it's okay with Dan, we're going to overlay some context, a.k.a., facts.

By the way, H/T RIGOP StrikeForce Co-Chair Mike Napolitano for highlighting this column. About the 27.5% income tax rate of the 1990's, Mike points out in comments under Dan's column that Rhode Island's income tax was calculated quite differently than it is today.

In fact, that rate was not based on the taxpayer’s income but on the taxpayer’s entire federal income tax liability. In other words if a taxpayer paid $100 in federal income tax they in turn paid $27.50 to the state of Rhode Island. The rate was piggybacked on to the federal rate and not on their wages.

So comparing 1997's 27.5% income tax rate to today's 5.99% rate is not valid at all because the former was a piggy back rate. (Imagine a state income tax that was 27.5% of your income. By the second year of such a rate, Rhode Island literally would no longer exist as a state.)

Now, with regard to Rhode Island's current top income tax rate of 5.99%, let's mosey on over to the Tax Foundation and click on the Rhode Island page.

Rhode Island's personal income tax system consists of three brackets and a top rate of 5.99%, kicking in at an income level of $129,900. Rhode Island's income tax system closely adheres to the federal income tax code. Among states levying personal income taxes, Rhode Island's top rate of 5.99% is the 3rd highest nationally.

Follow up question for Dan. Under his theory, how much higher would we have to make Rhode Island's top income tax for unemployment to start going back down? Obviously, it would have to go from number three nationally to number one. But by how much would we have to overshoot the current highest rate to get back to a decent unemployment rate?

Off topic ADDENDUM: To prove that I am not merely out to pick on GoLocalProv with this post, permit me to direct you to their very good story today about the star of that video released Saturday by the ProJo.

The man seen in an undercover video telling a campaign staffer for Congressional candidate Anthony Gemma that he could deliver mail ballot votes in exchange for $500 per week received a $103,000 taxpayer-funded loan for a restaurant from the city of Providence in 2004, GoLocalProv has learned.

Remember that Mr. Ramirez allegedly secured mail ballots for the David Cicilline campaign in a prior election. Now, who was mayor of Providence in 2004 when Mr. Ramirez' business secured this loan and who might have been feeling grateful for Mr. Ramirez' assistance to his campaign? Gosh, I'm trying to think ...

August 24, 2012

When I Grow Up, I Wanna Be a Crony

I can't confirm if this was filmed in Rhode Island or not (h/t):

"I'm gonna fight for MY piece of the taxpayer pie."

"What's a crony?"

"It's like having a best friend who gives you other people's stuff."

"We take care of our friends."

"We get to spend taxpayer money any way we want."

"Why be a taxpayer when I can be a tax spender?"

Yup, it had to be filmed here, right?

August 10, 2012

Legislative Votes For and Against Tolls on the Sakonnet River Bridge

Rhode Islanders, mainly from the East Bay, have organized a protest at Clements Market in Portsmouth, this afternoon, against tolls on the Sakonnet River Bridge. The hope is that the language that the General Assembly passed into law, this session, as Article 20 of the budget bill (7323Aaa) can be reversed.

That article and the budget to which it was attached were on the agendas of the RI House and Senate on June 7 and June 11, respectively. (The links are to the Ocean State Current's liveblogs, so readers can see who said what during debate.) In the Senate, Article 20 came up for a vote when Sen. Louis DiPalma (D, Little Compton, Middletown, Newport, Tiverton) proposed an amendment to remove it from the bill.

In the House, several amendments were raised and voted down to modify the article to make it less burdensome on local residents. The following table shows how the votes went in both chambers. The House voted on the article in three parts: Section 4, transferring the bridge's title to the RI Turnpike and Bridge Authority and authorizing tolls; parts of Section 3, authorizing the authority to maintain the bridge and set up tolls; and the rest of the article.

The votes below reflect the first vote, which is most explicit about tolls, but the article is written such that tolls would have been likely if any part of it passed. However, the only differences for the other two votes were that Baldelli-Hunt voted in favor of the language of Section 3, and Messier voted against the rest of the article.

July 19, 2012

Rhode Island To Offer Tax Amnesty

Governor Chafee's spokeswoman, Christine Hunsinger, confirmed this morning that one of the items in the FY2013 budget was a tax amnesty program. It will run from September 2 to November 15, 2012 and will apply to state taxes including income, sales, use, and unemployment insurance. Note that while monetary penalties and prosecution will be waived (for qualified applicants), interest would still be owed, albeit at a reduced rate.

More details from the CCH division of Wolters Kluwer Law & Business.

The program provides amnesty from penalties and from civil or criminal prosecution for any tax imposed under Rhode Island law and collected by the tax administrator for any taxable period ending on or before Dec. 31, 2011.Amnesty will be granted only to those taxpayers who apply on or before Nov. 15, who have paid the tax and interest due or who have entered into an installment payment agreement as a result of financial hardship.

Amnesty will not be granted to taxpayers who are under any criminal investigation or are a party to any civil or criminal proceeding pending in federal or Rhode Island court for fraud in relation to any state tax imposed.

As for how to apply, there appears to be nothing yet on the RI Division of Taxation's website; it is early. I left a message with an official at the Division of Taxation asking him how interested taxpayers would get started. When he calls back, I will post an update.

UPDATE

The Division of Taxation has advised that, as the start date of the program approaches, information will be made available on the Division's website for interested applicants.

July 17, 2012

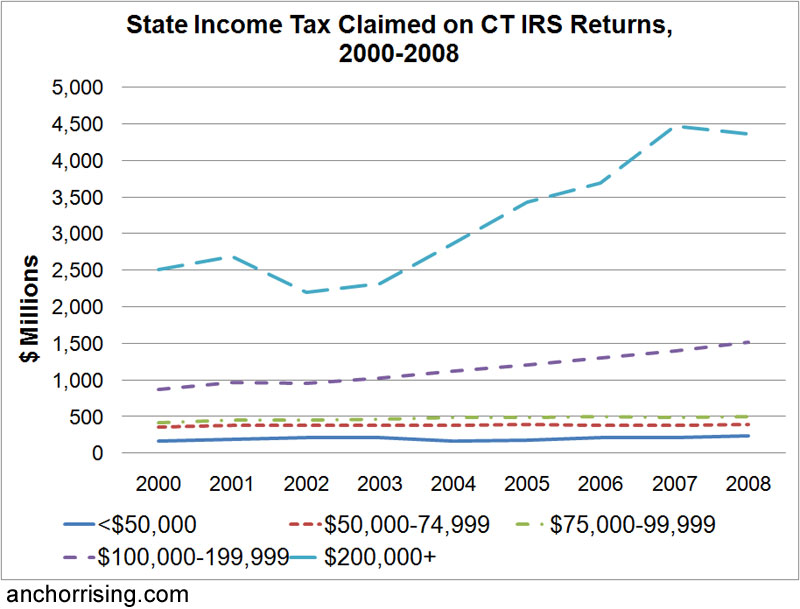

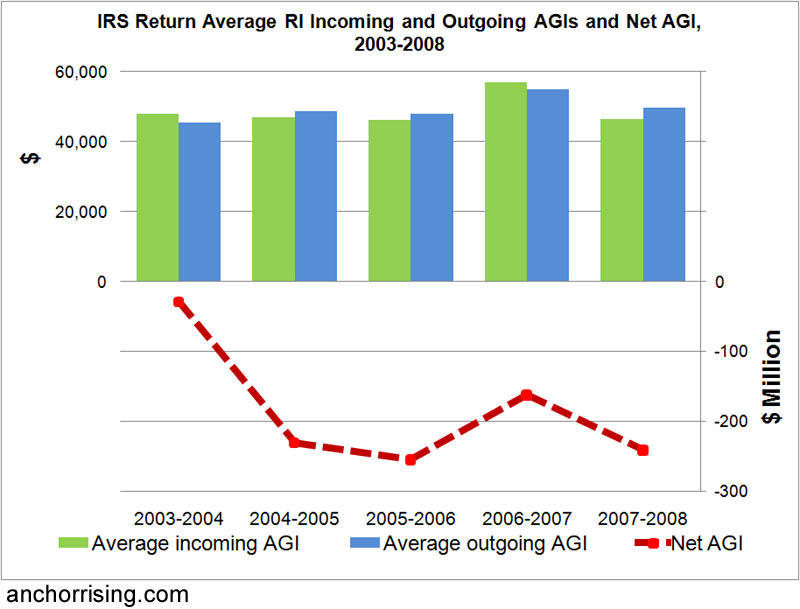

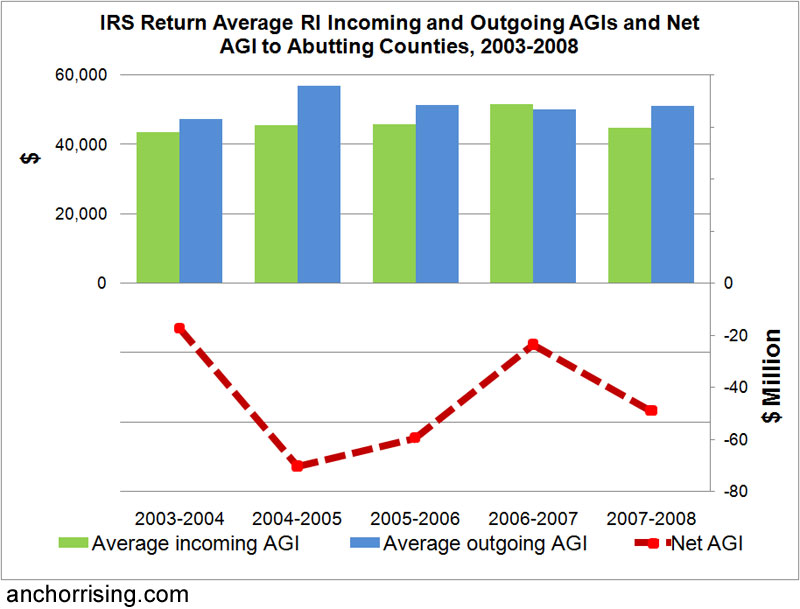

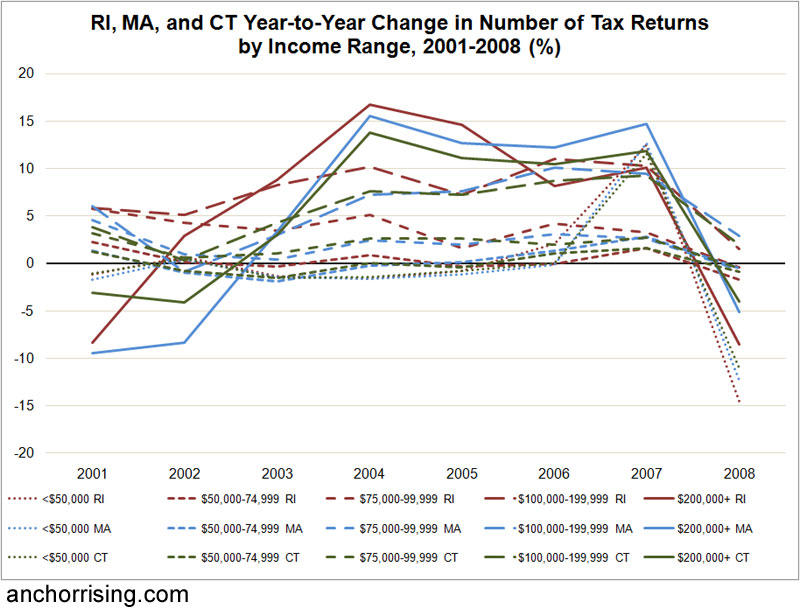

A Decade of Moving Next Door

I've been following taxpayer migration data for years, but in a haphazard way. A new study that I've coauthored for the RI Center for Freedom & Prosperity finally gave me the opportunity to review all fifteen years of available data from the IRS.

The picture — from the 2003 beginning of what can only be described as an exodus — is frightening. After accounting for the tens of thousands of Rhode Islanders who moved to other states and other taxpayers who moved in the opposite direction, Rhode Island lost 24,455 households, with $1.2 billion of annual income (not inflation adjusted). More conspicuously, a net 3,406 taxpayers moved right across the border, to abutting counties in Massachusetts and Connecticut, taking with them $254.5 million in annual adjusted gross income (AGI).

July 10, 2012

Small Business Getting the Screws

While President Obama attempts to frame the lapse of the "Bush tax cuts" in 2013 as a supposed return to the norm--with plenty of help from the media, who have accepted the premise that the extension of current tax rates are actually revenue "losses" should they be "extended"--he also recognizes that it would be political suicide to let that happen in toto. So he has come up with a plan to "extend" the "Bush tax cuts" another year for individuals making less than $200,000 and businesses making less than $250,000. According to the President, anyone making more will be taxed at the rate "we were paying under Bill Clinton." Not quite according to the Wall Street Journal:

[President Obama] ignores his ObamaCare tax increase of 0.9% on top of the current 2.9% Medicare tax, plus a new 2.9% surcharge on investment income, including interest income.How does this affect small business?That's an additional 3.8% surcharge on investment income, and added to the Bush expirations would take the capital gains rate to 23.8% from 15% today, and the dividend tax rate to about 45% from 15%. In Mr. Obama's economic world, tax cuts for middle-class "consumption" are good, but low rates to spur saving and investment are bad. This makes no sense because consumption is ultimately the product of saving and investment.

The President dismissed all of this as merely affecting 3% of small business owners. But that includes tens of thousands of the most productive, fastest-growing small businesses—those most likely to hire workers amid a national jobless rate of 8.2%.No, but the President--and the Federal Government--aren't as friendly to small business as they'd all like us to believe and it's nothing new, as the U.S. Small Business Administration reports:Congress's Joint Tax Committee—not a conservative outfit—estimates that in 2013 about 940,000 taxpayers will have enough business income to meet Mr. Obama's tax increase threshold. And of the roughly $1.3 trillion in net business income, about 53% will get hit with the higher tax rates.

This is because millions of businesses report their income as sole proprietors and subchapter S corporations that file under the individual tax code. So Mr. Obama wants these businesses to pay higher tax rates than the giant likes of General Electric or J.P. Morgan. Does that qualify as "tax fairness"?

The federal government last year fell short of its “small business” contracting goals for the eleventh straight year, a streak that stretches back to the first year of the George W. Bush administration. Federal agencies awarded contracts worth $91.5 billion to small companies in fiscal year 2011, equal to 21.7% of all prime government contract dollars awarded. Despite ongoing efforts to boost small business contracting, 2011 saw a drop of 6.5% from the 2010 total of $97.9 billion, which represented 22.7% of prime contract dollars. With a goal of 23%, however, the government came up short in both years, according to data released by the Small Business Administration (SBA).Couple the above with the way regulations are stacked against small-businesses, as Jay Carney explains in his analysis of a new policy paper arguing against corporatism (and for truly free markets) by Matt Mitchell, senior research fellow at George Mason University's Mercatus Center:

The government also failed to hit its contracting goals for businesses owned by women or service-disabled veterans, as well as for those located in traditionally underserved and underemployed regions of the country.

Politically favored businesses of course benefit from direct subsidies (think agribusiness) and government loan guarantees (think Solyndra and Boeing), but Mitchell makes the important point that regulation itself creates a privileged class.This is not an idea held by just free-market think tanks, either. Carney continues:Regulation often acts directly or indirectly as a barrier to entry. The conservative and libertarian media have documented this anecdotally -- Philip Morris supported and is benefiting from Obama's tobacco regulation, for instance, because the rules allow it to lock in its dominant market share.

For instance, liberal activists Ralph Nader and Mark Green wrote in the Yale Law Journal that the "regulatory system undermines competition and entrenches monopoly at the public's expense." Mitchell in this section also cites Alan Krueger, who now heads Obama's Council of Economic Advisers.Between regulation and higher taxes, it's no wonder that small-business owners feel like the screws are being put to them.In the Obama era, as Democrats and the media try to paint deregulation as some sort of dangerous sop to big business, Mitchell's notion of "regulatory privilege" is a crucial tool for dismantling the old narrative that regulation protects the public. Mitchell uses a colorful image to make his case: Bruce Yandle's "bootleggers and Baptists."

Illegal booze smugglers, Yandle wrote, "support Sunday closing laws that shut down all the local bars and liquor stores. Baptists support the same laws and lobby vigorously for them. Both parties gain. ..."

Rhode Island Is Not Delaware - Why Not?

I've been sitting on this article for a few days because I couldn't think of the best way to write about it. I guess in many ways, it's just so obvious that there isn't a whole lot to say. I'll just throw it out there.

On June 30, the NY Times published the article: How Delaware Thrives as a Corporate Tax Haven. The focus of the article seems to be the tax dodging and the criminal aspects of it. Some states, like Pennsylvania, get angry about Delaware's business-friendly tax laws and claim that Delaware robs them of their tax revenues.

State lawmakers in Pennsylvania are now trying to close the loophole, arguing that their state is being robbed of its tax dollars. Of particular concern is that many companies involved in drilling for natural gas in the Marcellus Shale region of Pennsylvania are, in fact, incorporating in Delaware instead.

“Delaware is an outlier in the way it does business,” said David E. Brunori, a professor at George Washington Law School and an expert on taxation. “What it offers is an opportunity to game the system and do it legally.”

Exactly, they do it legally. At least one state has set up an environment that is business-friendly to the point that many US corporations will actually seek it out to put an office there and pay tax dollars there. Even international entities will set up shop in Delaware due to their tax laws.

“Companies choose our state and we are proud of it,” said Richard J. Geisenberger, Delaware’s chief deputy secretary of state and its leading ambassador to business. “We spend a lot of time in the United States and traveling internationally to let people know that Delaware is a great place to do business.”

I'm sure some will turn up their nose at being "business friendly." It must come at the expense of everyone else, right? If you're going to be friendly to businesses, someone has to pick up the tax bill and the only alternative there is the lowly taxpayer. So let's take a look at Delaware's tax rates, especially in comparison to Rhode Island, using the Tax Foundation's numbers: DE RI

| State | Indiv. Income Tax Top Rate | Corporate Income Tax Flat Rate | Sales Tax | Property Tax Per Capita | Taxes Paid to State Per Capita | Unemployment rate |

| Delaware | 6.75% | 8.7% | 0% | $712 | $2,432* | 6.8% |

| Rhode Island | 5.99% | 9% | 7% | $2,019 | $3,290* | 11% |

*Total paid to the state is for 2009

According to those numbers, the residents of Delaware pay less in taxes and have an unemployment rate that's just a little bit more than half of Rhode Island's. Even better, they don't have a sales tax, so that will also attract residents of neighboring states into Delaware for puchases. Like I said earlier, this sort of thing is just so obvious, what else is there to say?

June 29, 2012

It's a Tax on Your Body

Unless I missed some language, the Supreme Court's ruling on ObamaCare shirks the responsibility of explicitly defining exactly what sort of tax Congress has imposed and how similar taxes might be structured in the future. Still, a thread can be followed.

Having just read through the tax-related sections of the ruling, and although the logic is as incoherent and slave to convenience as any I've ever read, it seems to me that a straightforward conclusion can be drawn.

First, on the incoherence: The health insurance mandate is apparently not a tax for determining the standing of the suit, but it is a tax to save the law. It's not a capitation tax — "a tax that everyone must pay simply for existing" — for the purpose of evading the constitutional requirement that such taxes be apportioned by state, but it's like a capitation tax for the purpose of evading precedent that prevents taxation from being used as stealth regulation. Bob and weave; whatever form it has to take to pass each obstacle.

However, in writing his opinion, Supreme Court Chief Justice John Roberts makes a big deal about the fact that people with no income tax burden do not have to pay the tax: "It does not apply to individuals who do not pay federal income taxes because their household income is less than the filing threshold in the Internal Revenue Code." Later, he likens it to a tax incentive.

The only way all of this makes coherent sense (which may be too high a standard for the highest court, granted) is if one takes the ruling a step farther to determine what sort of tax it is. I'd propose that the ObamaCare tax is effectively a capitation tax or a property tax on one's body.

June 27, 2012

Residential Property Tax Burdens in Rhode Island Municipalities

For reference from an upcoming post, but also interesting in its own right...

This table shows the residential property tax levy in each Rhode Island municipality, as a percentage of aggregate income in that municipality, as reported by the census bureau.

The details of residential property tax levy, involving the separation of residential from commercial property taxes (and treating apartment and mixed property tax classifications as residential, since much of that tax will be passed along to residential tenants), fire-district taxes and car-taxes, is explained here.

Community income in this chart is a single figure available from the Census Bureau's American Community Survey. This is a slightly different from the method I used last time where I presented this chart, where I multiplied per-capita income by total population figures taken from the ACS. Both methods give similar results.

The biggest gap in this chart is that the percentage of income paid in property tax in communities with many second vacation homes is inflated, since the income from non-residents is not included in the denominator.

As always, I'm open to further adjustments that can be made to these figures.

| Community | Estimated Residential Tax Levy (2011) | 2010 ACS Aggregate Household Income (2010) | % |

| New Shoreham | $7,548,403 | $44,124,500 | 17.1% |

| Westerly | $60,068,382 | $721,805,600 | 8.3% |

| Charlestown | $22,344,774 | $278,517,600 | 8.0% |

| Jamestown | $18,226,276 | $238,357,100 | 7.6% |

| Barrington | $52,531,961 | $751,029,500 | 7.0% |

| Smithfield | $44,556,739 | $637,479,200 | 7.0% |

| Narragansett | $41,330,974 | $598,013,000 | 6.9% |

| Hopkinton | $17,371,823 | $260,645,500 | 6.7% |

| Glocester | $20,367,277 | $307,319,000 | 6.6% |

| Tiverton | $32,555,171 | $493,782,200 | 6.6% |

| Foster | $10,126,928 | $155,949,200 | 6.5% |

| Cranston | $140,031,603 | $2,159,795,100 | 6.5% |

| North Providence | $55,663,407 | $877,310,000 | 6.3% |

| East Greenwich | $40,943,187 | $651,042,000 | 6.3% |

| South Kingstown | $59,666,885 | $960,168,600 | 6.2% |

| Little Compton | $9,690,006 | $156,354,200 | 6.2% |

| Scituate | $18,898,836 | $314,783,900 | 6.0% |

| Warren | $18,903,276 | $318,957,300 | 5.9% |

| Richmond | $14,284,170 | $241,437,600 | 5.9% |

| Coventry | $59,892,348 | $1,028,785,800 | 5.8% |

| North Smithfield | $22,118,882 | $380,866,900 | 5.8% |

| Portsmouth | $41,832,221 | $720,966,500 | 5.8% |

| Newport | $48,915,879 | $843,900,100 | 5.8% |

| Burrillville | $25,001,269 | $432,281,800 | 5.8% |

| Middletown | $31,522,496 | $548,112,800 | 5.8% |

| Warwick | $142,107,199 | $2,493,240,300 | 5.7% |

| North Kingstown | $57,562,579 | $1,034,986,400 | 5.6% |

| West Greenwich | $11,254,689 | $202,598,500 | 5.6% |

| Johnston | $40,940,330 | $749,941,000 | 5.5% |

| Providence | $187,919,289 | $3,489,797,500 | 5.4% |

| Exeter | $12,546,640 | $247,293,600 | 5.1% |

| East Providence | $64,344,891 | $1,280,295,600 | 5.0% |

| Cumberland | $55,052,263 | $1,098,496,100 | 5.0% |

| Pawtucket | $74,151,943 | $1,487,635,000 | 5.0% |

| Lincoln | $37,704,656 | $762,295,100 | 4.9% |

| Woonsocket | $38,789,267 | $812,621,300 | 4.8% |

| Bristol | $32,574,555 | $701,069,200 | 4.6% |

| West Warwick | $33,739,187 | $763,230,600 | 4.4% |

| Central Falls | $9,700,424 | $269,642,600 | 3.6% |

June 7, 2012

Who's Flying Now? (And Why?)

Ted Nesi posted an interesting graphic from the Tax Foundation that shows that:

Rhode Island posted the 18th-fastest growth in high-income taxpayers between 1999 and 2009.This prompted the NEA's Pat Crowley to chime in with a by-now familiar bit of rhetoric:While the total number of Rhode Island taxpayers grew by just 4% during that period, the number with adjusted gross incomes above $200,000 jumped 63%, for a net gain of 58.9% at the top end, the biggest in New England.

Vindication once again. The “flight of the earls” myth that was used as a justification to cut taxes on the elite in the middle part of the last decade is, once again, shown to be untrue.Well, as I responded, whether you believe in the "flight of the earls" theory or not (and setting aside that it's a bit of a strawman set up by Crowley anyway), the Tax Foundation chart and data doesn't really prove or disprove it at all because the data only compares the beginning and end of a time period in which RI cut the capital gains tax and enacted the flat tax (around 2006), which were aimed at keeping/attracting high earners. It’s just as possible that the "earls" were "flying" until the 2006 reforms and then we saw an influx. We’d have to see yearly data to more accurately determine causation/correlation. So let's do that.

First, even though what follows is a more robust way to look at the trend of higher income taxpayer migration, it is by no means comprehensive. It doesn't take inflation into account (though, as the Tax Foundation points out, their percentages are relative so that affect is mitigated in their analysis), which is why the relative increase in $200K wage-earning households when comparing 1999 to 2010 may be exaggerated. Additionally, the multitude of effects that the economic recession has had on wage-earners aren't adequately accounted for in this simplified manner.

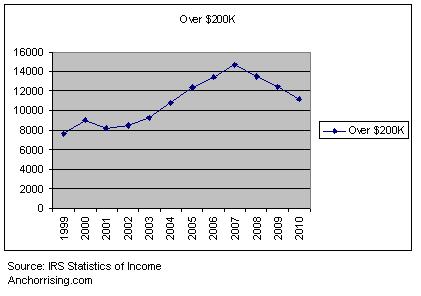

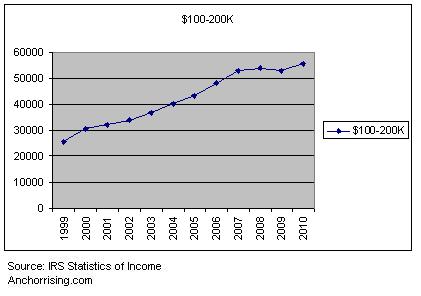

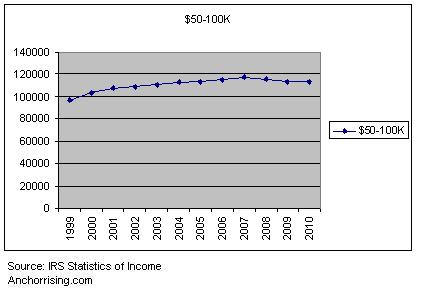

I turned to the IRS's Statistics on Income data from 1999-2010 and tallied up the number of + $200K taxpayers. (Yes, I thought I'd look at 2010, too).

Further, thanks to a timeline provided by Justin, we can compare the implementation of tax policies that were meant to impact high wage earners.

2002: capital gains tax phase-out passed to begin in 2007

2006: flat tax reduction begins

2007: capital gains tax phase-out begins with 2/3 reduction; then it's frozen

2010: capital gains tax increased to personal income level

2011: Flat tax rate reduction frozen

Keeping these dates in mind, let's look at the effects on + $200K wage-earning households. In 2000 there were 9,013 such taxpayers and this dropped to 8,259 in 2001, which, if memory serves, may have helped serve as an impetus for the tax policies that followed.

In 2002, when the capital gains tax phase-out was passed (to go into effect in 2007), the number of + $200K wage-earners went up to 8,500. From 2003 thru 2005, the numbers continued to increase, from 9,252 to 10,798 in 2004 to 12,376 in 2005. In 2006 the flat tax reduction begins and the climb continued to 13,387. In 2007, the capital gains tax phase-out begins with a 2/3 reduction of the previous level and the total + $200K wage-earning households climbed to 14,737. That year the General Assembly voted to freeze the capital gains tax (so the other 1/3 reduction did not occur) and the number dropped to 13,475 in 2008 and 12,416 in 2009. In 2009, the capital gains tax was set to be increased by matching it to personal income level in 2010. The number of households earning over $200K dropped to 11,117 in 2010. In 2011 the Flat tax rate reduction was frozen and we'll have to wait to see what happened.

When looking at the data for both "upper" middle-class and (I guess) "regular" middle-class, it looks like there is no relation between these tax policies and the number of wage earners.

For myself, I've been more of a "flight of the squires" kind of guy than "flight of the earls", believing that it's the middle-class who is suffering--and fleeing Rhode Island--more than the wealthy. As the above charts show, maybe that's wrong.

What I think this does show, however, is that there is a link between capital gains and flat tax policies and the impact they have on the number of high wage earners. During the time that these taxes were reduced, the number of + $200K wage-earners increased. After these taxes were frozen or raised, the number of + $200K wage-earners decreased.

ADDENDUM: The freeze/increase occurred before the economic downturn of 2008/2009 and, it looks like, the "earls" were already fleeing. It also looks like a lot of the "earls" became, um, "counts"(?), as the number of upper middle class wage earners seems to to be continually increasing, perhaps because some earls stayed in RI but dropped an income category. Also, the upper middle class is also being continually refreshed by regular middle class wage-earners moving up. In other words, it's important to remember that these classifications don't necessarily cover the same households.

May 19, 2012

What Is The Point Of Tax Credits?

A state will offer tax credits in order to incentivize a certain behavior that they wish. The holder of those credits then then use them to offset their own tax liability to the state. I have a friend who earns tax credits in various states by building affordable housing. Sometimes, his tax credits exceed his tax bill, so those credits become useless. Except, the state does allow the credits to be transferred. He'll then sell those earned credits to another business for cash and for less than the value of the credits. It's win-win-win. My friend wins because he gets cash, the other business wins because they're getting discounted money in the form of the credits and the state wins in that they get the affordable housing they desire.

Rhode Island has gotten into this game as well with the RI Film and TV Office. The state wanted to incentivize movies and television shows being made in Rhode Island, so they hand out tax credits for filming in RI and hiring Rhode Island businesses and citizens.

According to Ted Nesi, 38 Studios has applied for $12M in film tax credits for this year and has also submitted an application for $8.7M in credits for last year. So how in the world is 38 Studios going to justify applying for these tax credits? Are they going to get into the movie or television business now? The Film Office's definition of a motion picture does include video games, but only for theatrical or television purposes. I don't know that the definition fits.

If for some reason the state grants these requests, the only logical use for them is to sell them. Go back to the original scenario I described. A state wants a certain outcome, they incentivize it, someone grants the outcome and ends up with a surplus of credits in some instances. That's not what's seems to be happening here. It appears that 38 Studios would be applying for the tax credits for the sole purpose of selling them. If they plan to make a movie or television show and film it in RI with RI businesses and citizens, then great, give them the credits. If the sole purpose is to sell them, then no, the applications should not be approved.

During Governor Chafee's press conference yesterday, he also said that he will be proposing a bill that would cap the amount of tax credits to a single source at $5M. That's just in case you were wondering how the Governor felt about the state handing 38 Studios all this money.

I think if Chafee wants to go the distance on this one, add in that the credits cannot be transferred. Or, if that's too draconian, add in a provision that they cannot be transferred unless some portion of them (at least 50%?) have already been used by the requestor. To me, that makes perfect sense. It fits the original intended purpose of tax credits.

Bottom line, make a film or disallow the applications.

April 30, 2012

Businesses Go Where Taxes are Lower

Businesses will set up shop where the tax laws are more favorable to them.

And in other news, water is wet. Maybe it would seem obvious to most that people will be motivated by lower tax rates. However, if you listen to some on the left, especially locally, this isn't true. But how do you argue it when it comes straight from the horse's mouth?

“We set up in Luxembourg because of the favorable taxes,” said Robert Hatta, who helped oversee Apple’s iTunes retail marketing and sales for European markets until 2007.A New York Times article today "How Apple Sidesteps Billions In Taxes" tells much of the story and explains some of the various ways that Apple has chosen various places around the world to open offices, strictly due to the favorable tax laws. One of their offices has as few as twelve people assigned to it, but records revenues of one billion dollars a year.

It's not just international either. The California company even plays states off against each other.

Apple’s headquarters are in Cupertino, Calif. By putting an office in Reno, just 200 miles away, to collect and invest the company’s profits, Apple sidesteps state income taxes on some of those gains.If this can happen in a state as large as California, where 200 miles to Reno is considered "nearby", then can the same happen here where a 200 mile radius can land you in any of seven different states? Of course it can. It does! But yet, we still have those on the left who want to continually increase tax rates on businesses and further drive them away from Rhode Island.

California’s corporate tax rate is 8.84 percent. Nevada’s? Zero.

It's also interesting to see the outrage against Apple for paying so little in taxes or paying it to foreign countries or a state other than California, where they're headquartered. The NYT spoke with DeAnza College President Brian Murphy, as DeAnza is a nearby neighbor in Apple's hometown of Cupertino.

But the company’s tax policies are seen by officials like Mr. Murphy as symptomatic of why the crisis exists.I'd have a question for Mr. Murphy and anyone else who criticizes Apple for legally paying as few taxes as possible. Do you take the standard deduction on your tax return? Do you have children and claim them as a deduction? Do you take the mortgage interest deduction? Do you take charitable deductions or any other kinds? If so, what's the difference? Each of those are "loopholes" within the US tax law that we all legally take advantage of. Apple and many other corporations are merely doing the same.“I just don’t understand it,” he said in an interview. “I’ll bet every person at Apple has a connection to De Anza. Their kids swim in our pool. Their cousins take classes here. They drive past it every day, for Pete’s sake.

“But then they do everything they can to pay as few taxes as possible.”

If we don't like the loopholes, then we should close them. Work with those in Washington who make the tax laws and get them changed. In the meantime, let's see this for what it is, proof that businesses will go where the tax laws are favorable and at the same time ask ourselves, "How's business in Rhode Island?"

(h/t Ted Nesi)

March 8, 2012

Cities & Towns Appear Unwilling to Sign Onto Meals Tax Fools Bargain

As reported by the ProJo, many, many people testified before a House panel that was convened to discuss the new meals (and other) taxes being proposed by Governor Chafee. Purportedly, the money will be sent back to cities and towns, which caused the legislators to make an interesting observation.

Lawmakers, meanwhile, noted that no city or town officials testified in support of the tax plans, even though a significant chunk of the revenue would benefit their communities....“I found that pretty amazing,” House Finance Committee Chairman Helio Melo, D-East Providence, said afterward of the lack of support from cities and towns.Perhaps, just perhaps, cities and towns realize that this is a twofold fools bargain. What good is a raise in a tax if it can't be collected because its added cost caused the local business to close or move? And whose to say the money that is supposedly earmarked for cities and towns won't just end up elsewhere in the black hole of Rhode Island government?

Maybe a third reason is that they know every business is against it, so it's not a very politically popular stance to take, either. Well, for most people anyway:

The only person to testify in favor was Kate Brewster, executive director of the Economic Progress Institute, which advocates for policies affecting the poor....and never met a tax increase they didn't like. 'Nuff said.

March 5, 2012

Why RI Is Driving Out the Hushions

Jennifer Hushion submitted an op-ed to the Ocean State Current explaining why the City of Cranston and the state of Rhode Island are pushing her family toward the door:

The economic climate in Rhode Island — and specifically Cranston — is why we are considering leaving. It’s not that we are necessarily against higher taxes; we are against higher taxes when we receive so little in the way of services. Even more important to us than our current situation is the outlook for the future. Unfunded pension commitments and budget deficits are burying Cranston, and my family only sees the situation getting worse. ...I can understand why one might think that those who make over $250,000 are 'rich.' We have worked very hard and are grateful for what we have, but the math is undeniable. Spend 30% of taxable income on private education because of local schools’ inadequacy, pay another 10-15% in state property and income taxes, put another 15% away for a retirement that is slipping away, and being “rich” means driving an 11-year-old car and postponing badly needed household repairs.

March 4, 2012

Tax Surprise Time

It's tax time again and people are sitting with their 1040 and Schedule A and 1099 and W2 and all the other fun hoops the IRS makes you jump through. This year, it took me a minute but I was reminded of a little change to the RI tax code last year that very few people noticed.

Last June, with the fiscal mess the General Assembly was dealing with, they cooked up new ways to bring in revenue. One of those being to hold on to even more of our money. I normally get a pretty small refund from the state. My goal each year is to have both my tax returns end up as close to zero as possible. I don't want to have to pay anything more, but I don't want to give the government an interest-free loan either. However this year, we had no choice. The state decided that I can't afford to get back what I'm owed from the state. Or something. They've been withholding even more from each paycheck than they have in past years, even though they've already been withholding enough to result in a refund in past years.

On the face of it, it's a pleasant surprise to get a bigger refund than usual, but at the same time that money never should have been withheld from me in the first place. The state knows how much I need to pay them and I've been doing it just fine each year. Yet last year I needed to have even more withheld?

What the state did was give themselves an interest-free loan all year. If I missed my tax payments by the amount that Rhode Island missed their withholding, there'd be penalties involved. Interest added. But there's no interest in the other direction. Why?

Plus, there's the dumb economics of it. Let's say RI was withholding $40 a month too much from my paycheck. Let's also say I make the average salary and just to pick numbers out of the air, let's say there are 400,000 people working (eliminating the unemployed, retirees and underage). Just doing some back-of-the-napkin math, that's $1.6 million that the state has taken out of the economy each month or nearly $20 million over the last year. Does that make much sense? Our economy didn't need $20 million to be pumped in? I guess if they look at it selfishly and could get even a 2% return on that money, the state got a free $400,000 for simply holding on to it all year, only to give the $20 million back now. Not a bad deal, I guess.

Happy tax season.

February 24, 2012

The State of Local Taxation in Rhode Island, Measure II

How do amounts paid by municipal residents, in the form of local taxes, relate to how much their local governments have to spend?

Here is the answer for Rhode Island's cities and towns with the local tax levies measured in terms of percentage of income above a community's aggreggate poverty threshold...

The State of Local Taxation in Rhode Island, Measure I

How do amounts paid by municipal residents, in the form of local taxes, relate to how much their local governments have to spend?

Here is the answer for 38 Rhode Island cities and towns (New Shoreham is way off in the direction of the upper right-hand corner) with the local tax levy measured as a straight percentage of community aggregate income...

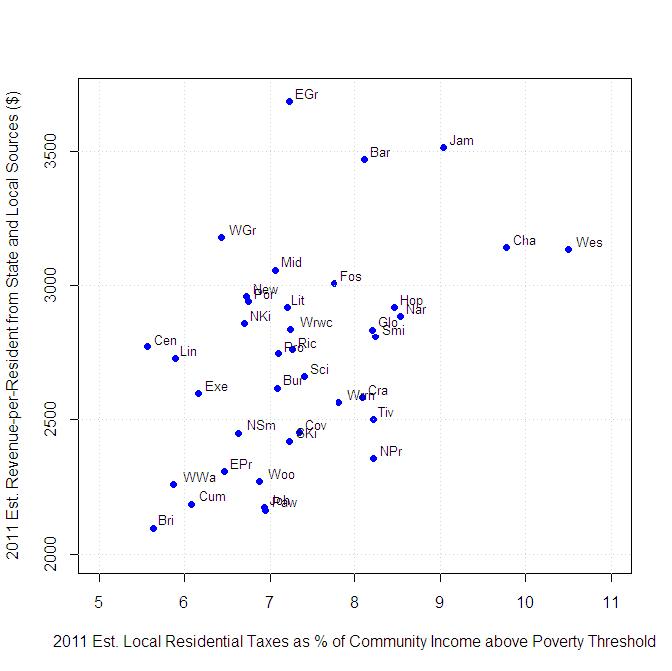

Revenue per Resident in Rhode Island Municipalities

While the percentage measures used in the previous posts provide initial insights into the question of willingness and ability to pay with regards to local taxation, the total picture requires looking at an absolute measure of what each RI city and town has available to spend, since the cost structure for local services is not a linear function of local income. For example the fact that per-capita income in North Providence is 80% of what it is in Foster does not mean that North Providence can provide the same services for 80% of what they cost in Foster.

Revenue from five sources for fiscal year 2011 (with the exception of the fire levies, noted below) is included in this table:

- The real property levy from all sources; residential, commercial and industrial.

- State non-education aid, which includes PILOT payments and the state car-tax reimbursement.

- Fire-district levies from all sources (using the 2010 data).

- Local car-tax levies.

- State education aid.

The amounts in each of the five categories for each city/town are below the fold, in Table 4.

Results are ranked using the sum of the five revenue sources per-capita...

| Community | Revenue From All Considered Sources | Population | Estimated Revenue per Resident |

| New Shoreham | $8,569,119 | 1,051 | $8,153 |

| East Greenwich | $48,431,608 | 13,146 | $3,684 |

| Jamestown | $18,984,613 | 5,405 | $3,512 |

| Barrington | $56,539,329 | 16,310 | $3,467 |

| West Greenwich | $19,504,001 | 6,135 | $3,179 |

| Charlestown | $24,593,699 | 7,827 | $3,142 |

| Westerly | $71,429,766 | 22,787 | $3,135 |

| Middletown | $49,407,769 | 16,150 | $3,059 |

| Foster | $13,860,749 | 4,606 | $3,009 |

| Newport | $73,014,485 | 24,672 | $2,959 |

| Portsmouth | $51,175,543 | 17,389 | $2,943 |

| Hopkinton | $23,912,807 | 8,188 | $2,920 |

| Little Compton | $10,196,191 | 3,492 | $2,920 |

| Narragansett | $45,773,136 | 15,868 | $2,885 |

| North Kingstown | $75,786,657 | 26,486 | $2,861 |

| Warwick | $234,713,634 | 82,672 | $2,839 |

| Glocester | $27,639,056 | 9,746 | $2,836 |

| Smithfield | $60,184,769 | 21,430 | $2,808 |

| Central Falls | $53,669,511 | 19,376 | $2,770 |

| Richmond | $21,284,730 | 7,708 | $2,761 |

| Providence | $488,555,304 | 178,042 | $2,744 |

| Lincoln | $57,568,015 | 21,105 | $2,728 |

| Scituate | $27,473,139 | 10,329 | $2,660 |

| Burrillville | $41,749,102 | 15,955 | $2,617 |

| Exeter | $16,680,553 | 6,425 | $2,596 |

| Cranston | $207,593,421 | 80,387 | $2,582 |

| Warren | $27,196,787 | 10,611 | $2,563 |

| Tiverton | $39,471,890 | 15,780 | $2,501 |

| Coventry | $85,874,992 | 35,014 | $2,453 |

| North Smithfield | $29,330,391 | 11,967 | $2,451 |

| South Kingstown | $74,173,165 | 30,639 | $2,421 |

| North Providence | $75,579,151 | 32,078 | $2,356 |

| East Providence | $108,554,357 | 47,037 | $2,308 |

| Woonsocket | $93,586,294 | 41,186 | $2,272 |

| West Warwick | $65,936,808 | 29,191 | $2,259 |

| Cumberland | $73,274,936 | 33,506 | $2,187 |

| Johnston | $62,572,597 | 28,769 | $2,175 |

| Pawtucket | $154,046,441 | 71,148 | $2,165 |

| Bristol | $48,178,255 | 22,954 | $2,099 |

Now, to put this all together...

Continue reading "Revenue per Resident in Rhode Island Municipalities"

February 23, 2012

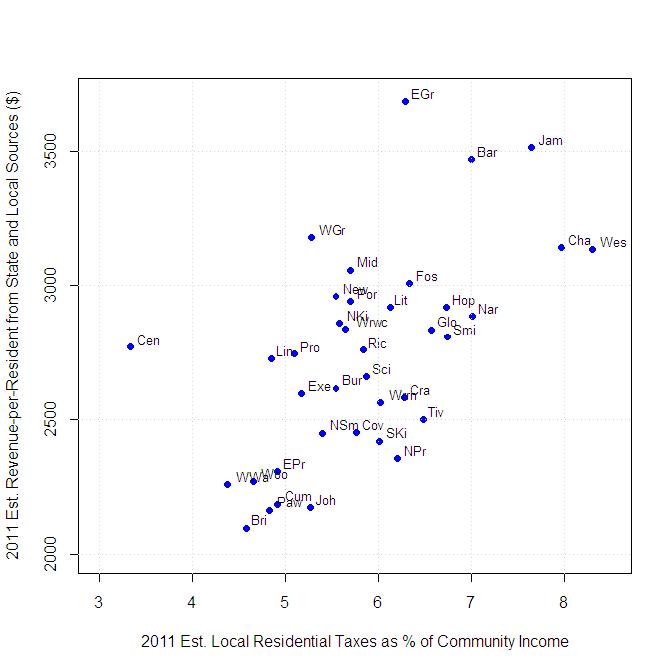

Residential Taxation in Rhode Island Municipalities, Part 2

In the previous post on local resident taxation in Rhode Island, there is a group of distressed communities (and Bristol?) at the bottom of the percentage-of-resident-income levied list. The clustering raises a question worth addressing of whether total income is the appropriate basis for measuring the taxation level in very poor communities.

The argument for adjusting the straight percentage is that there are certain fixed costs to human existence that are at least as important as paying your taxes and that taxation should be measured against what's left after basic necessities have been taken care of. The argument against is that an adequate adjustment has already built into a percentage metric, i.e. 5% of Central Falls' income would rank equally to 5% of New Shoreham's income on the straight-percentage list, even though it means much less money from Central Falls, and a further adjustment will open the divergence even wider.

I will calculate one version of a additional poverty adjustment, and present it along with the straight percentage measures going forward.

The Federal government annually calculates poverty thresholds based on family size. The Census Bureau's American Community Survey for 2010 includes a 5-year-based estimate of the number of households by number of household members in each RI community. Combining these two data elements, the amount of aggregate income needed to reach the Federal poverty threshold in each community can be estimated. Subtract that figure from the total estimated income in a community, and the result is estimated income above the poverty threshold.

The aggregate poverty thresholds alongside total community income for each Rhode Island community are listed below the fold in Table 3.

Using income-above-poverty-threshold as the percentage denominator does noticeably change the rankings. Pawtucket and Woonsocket, in particular, move up from the bottom of the list, though West Warwick and Central Falls stay about where they were...

| Community | Estimated Residential Taxes | Est. Community Income Above Poverty Threshold | % |

| New Shoreham | $7,548,403 | $43,156,924 | 17.5% |

| Westerly | $60,068,382 | $572,176,124 | 10.5% |

| Charlestown | $22,344,774 | $228,566,907 | 9.8% |

| Jamestown | $18,226,276 | $201,536,359 | 9.0% |

| Narragansett | $41,330,974 | $483,824,656 | 8.5% |

| Hopkinton | $17,371,823 | $205,331,075 | 8.5% |

| Smithfield | $44,556,739 | $540,793,934 | 8.2% |

| North Providence | $55,663,407 | $677,191,804 | 8.2% |

| Tiverton | $32,555,171 | $396,244,079 | 8.2% |

| Glocester | $20,367,277 | $248,135,004 | 8.2% |

| Barrington | $52,531,961 | $648,026,956 | 8.1% |

| Cranston | $140,031,603 | $1,731,101,472 | 8.1% |

| Warren | $18,903,276 | $242,159,186 | 7.8% |

| Foster | $10,126,928 | $130,700,587 | 7.7% |

| Scituate | $18,898,836 | $255,536,328 | 7.4% |

| Coventry | $59,892,348 | $816,146,172 | 7.3% |

| Richmond | $14,284,170 | $196,708,025 | 7.3% |

| Warwick | $142,107,199 | $1,962,582,789 | 7.2% |

| South Kingstown | $59,666,885 | $824,990,949 | 7.2% |

| East Greenwich | $40,943,187 | $567,021,673 | 7.2% |

| Little Compton | $9,690,006 | $134,548,069 | 7.2% |

| Providence | $187,919,289 | $2,645,403,886 | 7.1% |

| Burrillville | $25,001,269 | $352,665,391 | 7.1% |

| Middletown | $31,522,496 | $446,713,652 | 7.1% |

| Pawtucket | $74,151,943 | $1,067,974,255 | 6.9% |

| Johnston | $40,940,330 | $590,829,955 | 6.9% |

| Woonsocket | $38,789,267 | $563,406,119 | 6.9% |

| Portsmouth | $41,832,221 | $619,570,326 | 6.8% |

| Newport | $48,915,879 | $727,564,232 | 6.7% |

| North Kingstown | $57,562,579 | $859,563,071 | 6.7% |

| North Smithfield | $22,118,882 | $333,768,892 | 6.6% |

| East Providence | $64,344,891 | $996,042,498 | 6.5% |

| West Greenwich | $11,254,689 | $175,003,296 | 6.4% |

| Exeter | $12,546,640 | $203,667,786 | 6.2% |

| Cumberland | $55,052,263 | $905,804,162 | 6.1% |

| Lincoln | $37,704,656 | $640,511,273 | 5.9% |

| West Warwick | $33,739,187 | $574,321,052 | 5.9% |

| Bristol | $32,574,555 | $577,082,755 | 5.6% |

| Central Falls | $9,700,424 | $174,284,570 | 5.6% |